BarUpDn time limitedtrying to understand strategies, it appears that there is a lot of black magic in how a strat works behind the scenes.

anyway, it's hard to analyse what's all the data with one gazillion entries, and i wanted to know how we can manipulate/do stuff with a chart.

so, i needed to know how to "give" the script my values to work on. bundled two wants/needs into one, and created a script that only applies a strategy from the date given onwards.

how to use:

at the chart, go to the "format" little button, then the input tab, and there is all the date fields i created. fun to set it to the current date, then start going backwards and see all the little arrows filing up the chart :)

Cari dalam skrip untuk "the script"

Parabolic SAR Strategy with MACD Confirmation & Trend Zone Highl📝 Description (SEO + Follower-Friendly):

🚀 Powerful Trend Strategy Using Parabolic SAR + MACD

This advanced Pine Script combines the classic Parabolic SAR trend-following system with MACD crossover confirmation, improving entry precision and filtering out false signals. The script also features:

✅ Dynamic trend zone background highlighting when SAR is below price

✅ MACD filter ensures trades align with market momentum

✅ Custom SAR logic with adaptive acceleration

✅ Clean visual SAR plots for easy trend tracking

✅ Fully backtestable with strategy.entry logic

🔎 Ideal for traders seeking early trend entries, momentum confirmation, and visual clarity.

📈 Works on all timeframes and pairs — perfect for swing traders, scalpers, and crypto enthusiasts.

💡 Use it as a base strategy or combine with your favorite indicators.

❤️ If you find this helpful, don't forget to like, comment, and follow for more premium strategies!

SPXL Futures Strategy- Buy/sell signals for SPXL using futures momentum.

- For real-time signals at close, use ES1! on 2 minute chart and sign up for real-time cboe mini futures data feed in tradingview.

- All buys and sells are at near close of US RTH market at 4pm.

- Best to use the script with other breadth signals to decide on trading strategy.

- Script is compatible with SPY, SPXL, RSP, QQQ, TQQQ and many other SPX correlated tickers, however it’s primarily developed for SPX.

VWAP Bands BacktestThis is a backtest for evaluating the profitability of a vwap offsets strategy over time.

I took part of the code to create the script from Noro

So there is a link for its code

CCI strategy on OIL1HThis indicator is based on Commodity Channel Index.

It buys when CCI on period 200 is under -130 and it´s rising last 12 bars. It closes the position by hitting Take Profit, Stop Loss or opening short position.

It sells when CCI on period 200 is over 130 and it´s falling last 12 bars. It closes the position by hitting Take Profit, Stop Loss or opening short position.

This strategy seems to working just on USOIL on 1 hour chart. This can predict that it´s just luck and not proper strategy or indicator I would use for trading.

This script is just for educational purposes and that´s why the script is open. I will be happy if you will leave comment and try to come up with some ideas how to improve this strategy, so it can be used also on other commodities/forex pairs.

MarketCipher B Backtest (FOR TESTING ONLY, NOT SAFE TO TRADE)A script to backtest the strategy outlined. This is not a final version of the script and is therefore not safe to trade. If you choose to ignore this warning, trade at your own risk.

Ema BacktesterA simple, but useful script for backtesting purposes. Find the optimal Settings for your strategy.

tips are always welcome at: 38uGQJDDZDL6wX48x4gYTccPeQ3ZHVYmY4 (btc)

I hope you enjoy the script :)

BitMex Trailing Stop StrategyThis script is designed for those who want to use BitMex's trailing stop. It's not meant to be used as entry exits, but rather to get an idea of how wide the trailing stop needs to be. I suggest you backtest with different values. The script can also be integrated into an existing strategy which does give entry/exits to act as its stop loss.

Updated TurtlesThis script has been updated to prevent double orders (short/long) from occurring and modifying backtests results.

This is an update to the script that was written a few years ago to prevent double longs/shorts from occurring and skewin backtesting results. Check out the updated indicator here and let me know what you think.

I also added:

- date range inputs if you want to do some backtesting on a particular set of dates.

- the ability to toggle shorting

LFH/ Long positions using MACD histogram, long EMA and short EMADisclaimer: I'm a noob.

Hey there!

I'm trying to implement a script which enter market long position when long EMA crossover short EMA and MACD histogram is positive and histogram at T time is lesser than histogram at T-1.

And when short EMA crossover long EMA, plus MACD histogram is negative and histogram at T is greater than histogram at T-1, I want the script to exit market long position.

Now, I have something pretty close to what I am looking for. What I am missing and can't figure out yet is:

How to moderate entries, ie. I would like it to enter positions when trends are really interesting not just every time the conditions are fulfilled (same for exits) as there is way too much positions

I need to find a way to exit appropriated positions.

Another Millionaire toolBack with another Millionaire tool script, put like a solid 12 minutes here curve fitting the moving averages. THIS WILL MAKE YOU A MILLIONAIRE. It is so easy, it makes one of the hardest industries very very easy. Works on any market. I'VE DECIDED TO SHARE THE SCRIPT AND MAKE IT PUBLIC SO WE CAN ALL BE RICH TOGETHER, MILLIONAIRES

Reversal WaveThis is the type of quantitative system that can get you hated on investment forums, now that the Random Walk Theory is back in fashion. The strategy has simple price action rules, zero over-optimization, and is validated by a historical record of nearly a century on both Gold and the S&P 500 index.

Recommended Markets

SPX (Weekly, Monthly)

SPY (Monthly)

Tesla (Weekly)

XAUUSD (Weekly, Monthly)

NVDA (Weekly, Monthly)

Meta (Weekly, Monthly)

GOOG (Weekly, Monthly)

MSFT (Weekly, Monthly)

AAPL (Weekly, Monthly)

System Rules and Parameters

Total capital: $10,000

We will use 10% of the total capital per trade

Commissions will be 0.1% per trade

Condition 1: Previous Bearish Candle (isPrevBearish) (the closing price was lower than the opening price).

Condition 2: Midpoint of the Body The script calculates the exact midpoint of the body of that previous bearish candle.

• Formula: (Previous Open + Previous Close) / 2.

Condition 3: 50% Recovery (longCondition) The current candle must be bullish (green) and, most importantly, its closing price must be above the midpoint calculated in the previous step.

Once these parameters are met, the system executes a long entry and calculates the exit parameters:

Stop Loss (SL): Placed at the low of the candle that generated the entry signal.

Take Profit (TP): Calculated by projecting the risk distance upward.

• Calculation: Entry Price + (Risk * 1).

Risk:Reward Ratio of 1:1.

About the Profit Factor

In my experience, TradingView calculates profits and losses based on the percentage of movement, which can cause returns to not match expectations. This doesn’t significantly affect trending systems, but it can impact systems with a high win rate and a well-defined risk-reward ratio. It only takes one large entry candle that triggers the SL to translate into a major drop in performance.

For example, you might see a system with a 60% win rate and a 1:1 risk-reward ratio generating losses, even though commissions are under control relative to the number of trades.

My recommendation is to manually calculate the performance of systems with a well-defined risk-reward ratio, assuming you will trade using a fixed amount per trade and limit losses to a fixed percentage.

Remember that, even if candles are larger or smaller in size, we can maintain a fixed loss percentage by using leverage (in cases of low volatility) or reducing the capital at risk (when volatility is high).

Implementing leverage or capital reduction based on volatility is something I haven’t been able to incorporate into the code, but it would undoubtedly improve the system’s performance dramatically, as it would fix a consistent loss percentage per trade, preventing losses from fluctuating with volatility swings.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to exit or SL

And if volatility is high and exceeds the fixed percentage we want to expose per trade (if SL is hit), we could reduce the position size.

For example, imagine we only want to risk 15% per SL on Tesla, where volatility is high and would cause a 23.57% loss. In this case, we subtract 23.57% from 15% (the loss percentage we’re willing to accept per trade), then subtract the result from our usual position size.

23.57% - 15% = 8.57%

Suppose I use $200 per trade.

To calculate 8.57% of $200, simply multiply 200 by 8.57/100. This simple calculation shows that 8.57% equals about $17.14 of the $200. Then subtract that value from $200:

$200 - $17.14 = $182.86

In summary, if we reduced the position size to $182.86 (from the usual $200, where we’re willing to lose 15%), no matter whether Tesla moves up or down 23.57%, we would still only gain or lose 15% of the $200, thus respecting our risk management.

Final Notes

The code is extremely simple, and every step of its development is detailed within it.

If you liked this strategy, which complements very well with others I’ve already published, stay tuned. Best regards.

Adaptive Trend Navigator [ATH Filter & Risk Engine]Description:

This strategy implements a systematic Trend Following approach designed to capture major moves while actively protecting capital during severe bear markets. It combines a classic Moving Average "Fan" logic with two advanced risk management layers: a 4-Stage Dynamic Stop Loss and a macro-economic "Circuit Breaker" filter.

Core Concepts:

1. Trend Identification (Entry Logic) The script uses a cascade of Simple Moving Averages (SMA 25, 50, 100, 200) to identify the maturity of a trend.

Entries are triggered by specific crossovers (e.g., SMA 25 crossing SMA 50) or by breaking above the previous trade's high ("High-Water Mark" Re-Entry).

2. The "Circuit Breaker" (Crash Protection) To prevent trading during historical market collapses (like 2000 or 2008), the strategy monitors the Nasdaq 100 (QQQ) as a global benchmark:

Normal Regime: If the market is within 20% of its All-Time High, the strategy operates normally.

Crisis Regime: If the QQQ falls more than 20% from its ATH, the "Circuit Breaker" activates (Visualized by a Red Background).

Recovery Rule: In a Crisis Regime, new long positions are blocked unless the QQQ reclaims its SMA 200. This filters out "bull traps" in secular bear markets.

3. 4-Stage Risk Engine (Exit Logic) Once in a trade, the risk management adapts to the position's performance:

Stage 1: Fixed initial Stop Loss (default 10%) for breathing room.

Stage 2: Moves to Break-Even area once the price rises 12%.

Stage 3: Tightens to a trailing stop (8%) after 25% profit.

Stage 4: Maximizes gains with a tight trailing stop (5%) during parabolic moves (>40% profit).

Visual Guide:

SMAs: 25/50/100/200 period lines for trend visualization.

Red Background: Indicates the "Crisis Regime" where trading is halted due to broad market weakness.

Blue Background: Indicates a "Recovery Phase" (Crisis is active, but market is above SMA 200).

Red Line: Shows the dynamic Stop Loss level for active positions.

Settings: All parameters (SMA lengths, Drawdown threshold, Risk Stages) are fully customizable. The QQQ benchmark ticker can also be changed to SPY or other indices depending on the asset class traded.

Classic Wave: The Easy WayClassic Wave is a simple strategy with few rules and no over-optimization. Despite its simplicity, it is backed by a nearly century-long historical track record, delivering excellent returns on the weekly chart of the SPX (TVC).

I also recommend observing its strong performance on the SPY (weekly), which is the perfect instrument for executing this strategy with futures in the future.

Strategy Rules and Parameters

When a bullish candle closes above the 20-period EMA, we place the stop-loss below the low of that candle and target a risk-reward ratio of 1:1.

A second, more profitable variant is to change the risk-reward ratio in the code to 2:1.

-Total capital: $10,000

-We use 10% of the total capital per trade.

-Commissions: 0.1% per trade.

The code construction is simple and very well detailed within the script itself.

Risk-Reward Ratio 2:1

Using a 2:1 risk-reward ratio reduces the win rate but significantly increases profitability.

Across the full historical data of the SPX index (weekly), the system would have generated 236 trades, with a win rate of 51.27% and a profit factor of 2.53.

From January 1, 2023, to November 28, 2025, the system would have generated 5 trades, with an 80% win rate and a profit factor of 9.244.

What makes this system so good?

-It takes advantage of the long-term bullish bias of U.S. stock indices and traditional markets.

-It filters out a lot of noise thanks to the weekly timeframe.

-It uses simple parameters with no over-optimization.

Final Notes:

This strategy has consistently outperformed the returns offered by most traditional funds over time, with fewer drawdowns and significantly less stress. I hope you like it.

Long-Term Strategy: 1-Year Breakout + 6-Month ExitDescripción (Description): (Copia y pega todo lo que está dentro del recuadro de abajo)

Description

This is a long-term trend-following strategy designed to capture major market moves while filtering out short-term noise. It is based on the classic principle of "buying strength" (Breakouts) and allowing profits to run, while cutting losses when the medium-term trend reverses.

How it Works (Logic)

1. Entry Condition (Long Only): The strategy looks for a significant display of strength. It enters a Long position only when two conditions are met simultaneously:

Price Breakout: The closing price exceeds the highest high of the last 252 trading days (approximately 1 year). This ensures we are entering during a strong momentum phase.

Trend Filter: The SuperTrend indicator (Settings: ATR 10, Factor 3.0) must be bullish. This acts as a confirmation filter to avoid false breakouts in choppy markets.

2. Exit Condition: The strategy uses a trailing stop based on price action, not a fixed percentage.

It closes the position when the price closes below the lowest low of the last 126 trading days (approximately 6 months).

This wide exit allows the trade to "breathe" during normal market corrections without exiting the position prematurely.

Settings & Risk Management

Capital Usage: The script is configured to use 10% of equity per trade to reflect realistic risk management (compounding).

Commissions: Included at 0.1% to simulate real trading costs.

Slippage: Included (3 ticks) to account for market execution variability.

Best Use: This strategy is intended for higher timeframes (Daily or Weekly) on trending assets like Indices, Crypto, or Commodities.

Qullamagi EMA Breakout Autotrade (Crypto Futures L+S)Title: Qullamagi EMA Breakout – Crypto Autotrade

Overview

A crypto-focused, Qullamagi-style EMA breakout strategy built for autotrading on futures and perpetual swaps.

It combines a 5-MA trend stack (EMA 10/20, SMA 50/100/200), volatility contraction boxes, volume spikes and an optional higher-timeframe 200-MA filter. The script supports both long and short trades, partial take profit, trailing MA exits and percent-of-equity position sizing for automated crypto futures trading.

Key Features (Crypto)

Qullamagi MA Breakout Engine – trades only when price is aligned with a strong EMA/SMA trend and breaks out of a tight consolidation range. Longs use: Close > EMA10 > EMA20 > SMA50 > SMA100 > SMA200. Shorts are the mirror condition with all MAs sloping in the trend direction.

Strict vs Loose Modes – Strict (Daily) is designed for cleaner swing trades on 1H–4H (full MA stack, box+ATR and volume filters, optional HTF filter). Loose (Intraday) focuses on 10/20/50 alignment with relaxed filters for more frequent 15m–30m signals.

Volatility & Volume Filters for Crypto – ATR-based box height limit to detect volatility contraction, wide-candle filter to avoid chasing exhausted breakouts, and a volume spike condition requiring current volume to exceed an SMA of volume.

Higher-Timeframe Trend Filter (Optional) – uses a 200-period SMA on a higher timeframe (default: 1D). Longs only when HTF close is above the HTF 200-SMA, shorts only when it is below, helping avoid trading against dominant crypto trends.

Autotrade-Oriented Trade Management – position size as % of equity, initial stop anchored to a chosen MA (EMA10 / EMA20 / SMA50) with optional buffer, partial take profit at a configurable R-multiple, trailing MA exit for the remainder, and an optional cooldown after a full exit.

Markets & Timeframes

Best suited for BTC, ETH and major altcoin futures/perpetuals (Binance, Bybit, OKX, etc.).

Strict preset: 1H–4H charts for classic Qullamagi-style trend structure and fewer fake breakouts.

Loose preset: 15m–30m charts for higher trade frequency and more active intraday trading.

Always retune ATR length, box length, volume multiplier and position size for each symbol and exchange.

Strategy Logic (Quick Summary)

Long (Strict): MA stack in bullish alignment with all MAs sloping up → tight volatility box (ATR-based) → volume spike above SMA(volume) × multiplier → breakout above box high (close or intrabar) → optional HTF close above 200-SMA.

Short: Mirror logic: bearish MA stack, tight box, volume spike and breakdown below box low with optional HTF downtrend.

Best Practices for Crypto

Backtest on each symbol and timeframe you plan to autotrade, including commissions and slippage.

Start on higher timeframes (1H/4H) to learn the behavior, then move to 15m–30m if you want more signals.

Use the higher-timeframe filter when markets are strongly trending to reduce counter-trend trades.

Keep position-size percentage conservative until you fully understand the drawdowns.

Forward-test / paper trade before connecting to live futures accounts.

Webhook / Autotrade Integration

Designed to work with TradingView webhooks and external crypto trading bots.

Alert messages include structured fields such as: EVENT=ENTRY / SCALE_OUT / EXIT, SIDE=LONG / SHORT, STRATEGY=Qullamagi_MA.

Map each EVENT + SIDE combination to your bot logic (open long/short, partial close, full close, etc.) on your preferred exchange.

Important Notes & Disclaimer

Crypto markets are highly volatile and can change regime quickly. Backtest and forward-test thoroughly before using real capital. Higher timeframes generally produce cleaner MA structures and fewer fake breakouts.

This strategy is for educational and informational purposes only and does not constitute financial advice. Trading leveraged crypto products involves substantial risk of loss. Always do your own research, manage risk carefully, and never trade with money you cannot afford to lose.

RSI + MACD Multi-Timeframe StrategyThis strategy combines the Relative Strength Index (RSI) from the daily timeframe with the Moving Average Convergence Divergence (MACD) from the 4-hour timeframe to generate precise long entry and exit signals.

The system uses a multi-timeframe approach to align longer-term trend conditions with shorter-term momentum shifts — allowing traders to catch dips with confirmation and exit before reversals.

🧠 Strategy Logic

✅ Long Entry Condition:

- RSI on the daily (1D) timeframe is oversold (below your defined threshold)

- MACD on the 4H timeframe crosses above the signal line

→ A long trade is opened when these two align

✅ Long Exit Condition:

- RSI on the daily timeframe is overbought

- MACD on the 4H timeframe crosses below the signal line

→ The long trade is closed when these two conditions are met

💡 This strategy currently supports long entries only. Short logic can be added if needed.

📊 Indicator Components

🔹 RSI (Relative Strength Index):

- A momentum oscillator that measures the speed and magnitude of price changes.

- Helps identify overbought (potential sell) and oversold (potential buy) conditions.

- Applied on the 1D timeframe (by default) to reflect broader market trend or exhaustion levels.

🔹 MACD (Moving Average Convergence Divergence):

- A trend-following momentum indicator based on moving averages.

- The MACD Line (fast EMA - slow EMA) crossing above the Signal Line indicates bullish momentum.

- Used here on the 4-hour timeframe (by default) for shorter-term momentum confirmation.

🔹 Multi-Timeframe (MTF) Logic:

- Uses request.security() to pull higher timeframe data (1D for RSI, 4H for MACD).

- Ensures no repainting, as it only uses closed candles from the higher timeframe.

- Aligns longer-term signals with shorter-term entries, reducing false signals.

📈 Plotting Options

The script includes a plot selector input allowing you to toggle between:

- RSI Plot (with overbought/oversold lines)

- MACD Plot (MACD line and signal line)

- This helps visualize signal conditions clearly on your chart.

🛠 Customization

- RSI & MACD settings are fully configurable

- RSI and MACD timeframes can be adjusted independently

⚠️ Disclaimer

This strategy is provided for educational and informational purposes only.

It is not financial advice or a recommendation to buy or sell any asset.

Past performance does not guarantee future results. Always test strategies in a simulated environment before live use, and consult with a licensed financial advisor for investment decisions.

Gold H1 Breakout Failure (V11.0)This strategy is designed for trading XAU/USD (Gold) on the 1-hour timeframe. It identifies and trades fake breakouts of the Asian session range.

The logic is simple yet effective:

The script first marks the Asian session high and low.

Once price breaks out of this range and closes outside, it waits for confirmation by watching for price to close back inside the range.

When this re-entry occurs, the strategy takes a position in the opposite direction of the initial breakout, anticipating a false breakout or liquidity trap setup.

By focusing on these fakeouts, the strategy aims to capture reversal momentum after liquidity sweeps, making it especially effective during sessions when volatility transitions from Asia to London or New York.

NLR-ADX Divergence Strategy Triple-ConfirmedHow it works

Builds a cleaner DMI/ADX

Recomputes classic +DI, −DI, ADX over a user-set length.

Then “non-linear regresses” each series toward a mean (your choice: dynamic EMA of the series or a fixed Static Mid like 50).

The further a value is from the mean, the stronger the pull (controlled by alphaMin/alphaMax and the γ exponent), giving smoother, more stable DI/ADX lines with less whipsaw.

Optional EMA smoothing on top of that.

Lock in values at confirmed pivots

Uses price pivots (left/right bars) to confirm swing lows and highs.

When a pivot confirms, the script captures (“freezes”) the current +DI, −DI, and ADX values at that bar and stores them. This avoids later drift from smoothing/EMAs.

Check for triple divergence

For a bullish setup (potential long):

Price makes a Lower Low vs. a prior pivot low,

+DI is higher than before (bulls quietly stronger),

−DI is lower (bears weakening),

ADX is lower (trend fatigue).

For a bearish setup (potential short)

Price makes a Higher High,

+DI is lower, −DI is higher,

ADX is lower.

Adds a “no-intersection” sanity check: between the two pivots, the live series shouldn’t snake across the straight line connecting endpoints. This filters messy, low-quality structures.

Trade logic

On a valid triple-confirm, places a strategy.entry (Long for bullish, Short for bearish) and optionally labels the bar (BUY or SELL with +DI/−DI/ADX arrows).

Simple flip behavior: if you’re long and a new short signal prints (or vice versa), it closes the open side and flips.

Key inputs you can tweak

Custom DMI Settings

DMI Length — base length for DI/ADX.

Non-Linear Regression Model

Mean Reference — EMA(series) (dynamic) or Static mid (e.g., 50).

Dynamic Mean Length & Deviation Scale Length — govern the mean and scale used for regression.

Min/Max Regression & Non-Linearity Exponent (γ) — how strongly values are pulled toward the mean (stronger when far away).

Divergence Engine

Pivot Left/Right Bars — how strict the swing confirmation is (larger = more confirmation, more delay).

Min Bars Between Pivots — avoids comparing “near-duplicate” swings.

Max Historical Pivots to Store — memory cap.

ICT Liquidity Sweep Asia/London 1 Trade per High & Low🧠 ICT Liquidity Sweep Asia/London — 1 Trade per High & Low

This strategy is inspired by the ICT (Inner Circle Trader) concepts of liquidity sweeps and market structure, focusing on the Asia and London sessions.

It automatically identifies liquidity grabs (sweeps) above or below key session highs/lows and enters trades with a fixed risk/reward ratio (RR).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚙️ Core Logic

-Asia Session: 8:00 PM – 11:59 PM (New York time)

-London Session: 2:00 AM – 5:00 AM (New York time)

-The script marks the Asia High/Low and London High/Low ranges for each day.

-When the market sweeps above a session high → potential Short setup

-When the market sweeps below a session low → potential Long setup

-A trade is triggered when the confirmation candle closes in the opposite direction of the sweep (bearish after a high sweep, bullish after a low sweep).

-Only one trade per sweep type (1 per High, 1 per Low) is allowed per session.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

📈 Risk Management

-Configurable Risk/Reward Target (default = 2:1)

-Configurable Position Size (number of contracts)

-Each trade uses a fixed Stop Loss (beyond the wick of the sweep) and a Take Profit calculated from the RR setting.

-All trades are automatically logged in the Strategy Tester with performance metrics.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

💡 Features

✅ Visual session highlighting (Asia = Aqua, London = Orange)

✅ Automatic liquidity line plotting (session highs/lows)

✅ Entry & exit labels (optional visual display)

✅ Customizable RR and contract size

✅ Works on any instrument (ideal for indices, futures, or forex)

✅ Compatible with all timeframes (optimized for 1M–15M)

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚠️ Notes

-Best used on New York time-based charts.

-Designed for educational and backtesting purposes — not financial advice.

-Use as a foundation for further optimization (e.g., SMT confirmation, FVG filter, or time-based restrictions).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

🧩 Recommended Use

Pair this with:

-ICT’s concepts like CISD (Change in State of Delivery) and FVGs (Fair Value Gaps)

-Higher timeframe liquidity maps

-Session bias or daily narrative filters

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

Author: jygirouard

Strategy Version: 1.3

Type: ICT Liquidity Sweep Automation

Timezone: America/New_York

USDJPY Fair Value Gap + Session Strategy🎯 Overview

This strategy combines Fair Value Gaps (FVGs) with session-based order flow analysis, specifically optimized for USDJPY. It identifies price inefficiencies left behind by institutional order flow during high-volatility trading sessions, offering a modern alternative to traditional lagging indicators.

🔬 What Are Fair Value Gaps?

Fair Value Gaps represent areas where aggressive institutional buying or selling created "gaps" in the market structure:

Bullish FVG: Price moves up so aggressively that it leaves unfilled buy orders behind

Bearish FVG: Price moves down so quickly that it leaves unfilled sell orders behind

Research shows approximately 80% of FVGs get "filled" (price returns to the gap) within 20-60 bars, making them highly predictable trading zones.

(see the generated image above)

(see the generated image above)

FVG Detection Logic:

text

// Bullish FVG: Gap between high and current low

bullishFVG = low > high and high > high

// Bearish FVG: Gap between low and current high

bearishFVG = high < low and low < low

🌏 Session-Based Trading

Why Sessions Matter for USDJPY

(see the generated image above)

Tokyo Session (00:00-09:00 UTC)

Highest volatility during first hour (00:00-01:00 UTC)

Average movement: 51-60 pips

Best for breakout strategies

London/NY Overlap (13:00-16:00 UTC)

Maximum liquidity and institutional participation

Tightest spreads and most reliable FVG formations

Optimal for continuation trades

Monday Premium Effect

USDJPY moves 120+ pips on Mondays due to weekend positioning

Enhanced FVG formation during session opens

📊 Strategy Components

(see the generated image above)

1. Fair Value Gap Detection

Identifies bullish and bearish FVGs automatically

Age limit: FVGs expire after 20 bars to avoid stale setups

Size filter: Minimum gap size to filter out noise

2. Session Filtering

Tokyo Open focus: Trades during first hour of Asian session

London/NY Overlap: Captures high-liquidity institutional flows

Weekend gap strategy: Enhanced signals on Monday opens

3. Volume Confirmation

Requires 1.5x average volume spike

Confirms institutional participation

Reduces false signals

4. Trend Alignment

50 EMA filter ensures trades align with higher timeframe trend

Long trades above EMA, short trades below

Prevents costly counter-trend trades

5. Risk Management

2:1 Risk/Reward minimum ensures profitability with 40%+ win rate

Percentage-based stops adapt to USDJPY volatility (0.3% default)

Configurable position sizing

🎯 Entry Conditions

(see the generated image above)

Long Entry (BUY)

✅ Bullish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price above 50 EMA (trend confirmation)

✅ Bullish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

Short Entry (SELL)

✅ Bearish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price below 50 EMA (trend confirmation)

✅ Bearish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

📈 Expected Performance

Backtesting Results (Based on Similar Strategies):

Win Rate: 44-59% (profitable due to high R:R ratio)

Average Winner: 60-90 pips during London/NY sessions

Average Loser: 30-40 pips (tight stops at FVG boundaries)

Risk/Reward: 2:1 minimum, often 3:1 during strong trends

Best Performance: Monday Tokyo opens and Wednesday London/NY overlaps

Why This Works for USDJPY:

90% correlation with US-Japan bond yield spreads

High volatility provides sufficient pip movement

Heavy institutional/central bank participation creates clear FVGs

Consistent volatility patterns across trading sessions

⚙️ Configurable Parameters

Session Settings:

Trade Tokyo Session (Enable/Disable)

Trade London/NY Overlap (Enable/Disable)

FVG Settings:

FVG Minimum Size (Filter small gaps)

Maximum FVG Age (20 bars default)

Show FVG Markers (Visual display)

Volume Settings:

Use Volume Filter (Enable/Disable)

Volume Multiplier (1.5x default)

Volume Average Period (20 bars)

Trend Settings:

Use Trend Filter (Enable/Disable)

Trend EMA Period (50 default)

Risk Management:

Risk/Reward Ratio (2.0 default)

Stop Loss Percentage (0.3% default)

🎨 Visual Indicators

🟡 Yellow Line: 50 EMA trend filter

🟢 Green Triangles: Long entry signals

🔴 Red Triangles: Short entry signals

🟢 Green Dots: Bullish FVG zones

🔴 Red Dots: Bearish FVG zones

🟦 Blue Background: Tokyo open session

🟧 Orange Background: London/NY overlap

📊 Recommended Settings

Optimal Timeframes:

Primary: 5-minute charts (scalping)

Secondary: 15-minute charts (swing trading)

Parameter Optimization:

Conservative: Stop Loss 0.2%, R:R 2:1, Volume 2.0x

Balanced: Stop Loss 0.3%, R:R 2:1, Volume 1.5x (default)

Aggressive: Stop Loss 0.4%, R:R 1.5:1, Volume 1.2x

Risk Management:

Maximum 1-2% of account per trade

Daily loss limit: Stop after 3-5 consecutive losses

Use fixed percentage position sizing

⚠️ Important Considerations

Avoid Trading During:

Major news events (BOJ interventions, NFP, FOMC)

Holiday periods with reduced liquidity

Low volatility Asian afternoon sessions

When US-Japan yield differential narrows sharply

Best Practices:

Limit to 2-3 trades per session maximum

Always respect the 50 EMA trend filter

Never risk more than planned per trade

Paper trade for 2-4 weeks before live implementation

Track performance by session and day of week

🚀 How to Use

Add the script to your USDJPY chart

Set timeframe to 5-minute or 15-minute

Adjust parameters based on your risk tolerance

Enable strategy alerts for automated notifications

Wait for visual signals (triangles) to appear

Enter trades according to your risk management rules

📚 Strategy Foundation

This strategy is based on:

Smart Money Concepts (SMC): Institutional order flow tracking

Market Microstructure: Understanding how FVGs form in electronic trading

Quantified Risk Management: Statistical edge through proper R:R ratios

Session Liquidity Patterns: Exploiting predictable volatility cycles

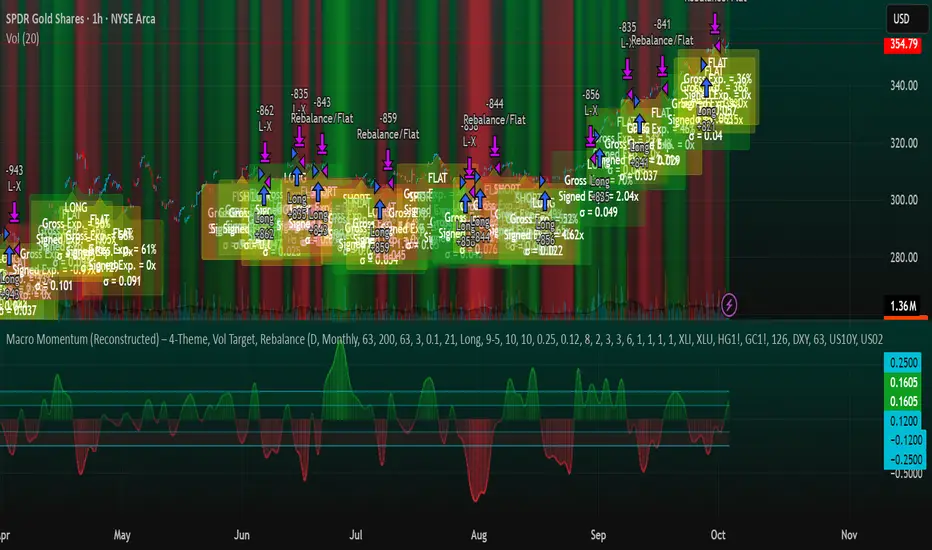

Macro Momentum – 4-Theme, Vol Target, RebalanceMacro Momentum — 4-Theme, Vol Target, Rebalance

Purpose. A macro-aware strategy that blends four economic “themes”—Business Cycle, Trade/USD, Monetary Policy, and Risk Sentiment—into a single, smoothed Composite signal. It then:

gates entries/exits with hysteresis bands,

enforces optional regime filters (200-day bias), and

sizes the position via volatility targeting with caps for long/short exposure.

It’s designed to run on any chart (index, ETF, futures, single stocks) while reading external macro proxies on a chosen Signal Timeframe.

How it works (high level)

Build four theme signals from robust macro proxies:

Business Cycle: XLI/XLU and Copper/Gold momentum, confirmed by the chart’s price vs a long SMA (default 200D).

Trade / USD: DXY momentum (sign-flipped so a rising USD is bearish for risk assets).

Monetary Policy: 10Y–2Y curve slope momentum and 10Y yield trend (steepening & falling 10Y = risk-on; rising 10Y = risk-off).

Risk Sentiment: VIX momentum (bearish if higher) and HYG/IEF momentum (bullish if credit outperforms duration).

Normalize & de-noise.

Optional Winsorization (MAD or stdev) clamps outliers over a lookback window.

Optional Z-score → tanh mapping compresses to ~ for stable weighting.

Theme lines are SMA-smoothed; the final Composite is LSMA-smoothed (linreg).

Decide direction with hysteresis.

Enter/hold long when Composite ≥ Entry Band; enter/hold short when Composite ≤ −Entry Band.

Exit bands are tighter than entry bands to avoid whipsaws.

Apply regime & direction constraints.

Optional Long-only above 200MA (chart symbol) and/or Short-only below 200MA.

Global Direction control (Long / Short / Both) and Invert switch.

Size via volatility targeting.

Realized close-to-close vol is annualized (choose 9-5 or 24/7 market profile).

Target exposure = TargetVol / RealizedVol, capped by Max Long/Max Short multipliers.

Quantity is computed from equity; futures are rounded to whole contracts.

Rebalance cadence & execution.

Trades are placed on Weekly / Monthly / Quarterly rebalance bars or when the sign of exposure flips.

Optional ATR stop/TP for single-stock style risk management.

Inputs you’ll actually tweak

General

Signal Timeframe: Where macro is sampled (e.g., D/W).

Rebalance Frequency: Weekly / Monthly / Quarterly.

ROC & SMA lengths: Defaults for theme momentum and the 200D regime filter.

Normalization: Z-score (tanh) on/off.

Winsorization

Toggle, lookback, multiplier, MAD vs Stdev.

Risk / Sizing

Target Annualized Vol & Realized Vol Lookback.

Direction (Long/Short/Both) and Invert.

Max long/short exposure caps.

Advanced Thresholds

Theme/Composite smoothing lengths.

Entry/Exit bands (hysteresis).

Regime / Execution

Long-only above 200MA, Short-only below 200MA.

Stops/TP (optional)

ATR length and SL/TP multiples.

Theme Weights

Per-theme scalars so you can push/pull emphasis (e.g., overweight Policy during rate cycles).

Macro Proxies

Symbols for each theme (XLI, XLU, HG1!, GC1!, DXY, US10Y, US02Y, VIX, HYG, IEF). Swap to alternatives as needed (e.g., UUP for DXY).

Signals & logic (under the hood)

Business Cycle = ½ ROC(XLI/XLU) + ½ ROC(Copper/Gold), then confirmed by (price > 200SMA ? +1 : −1).

Trade / USD = −ROC(DXY).

Monetary Policy = 0.6·ROC(10Y–2Y) − 0.4·ROC(10Y).

Risk Sentiment = −0.6·ROC(VIX) + 0.4·ROC(HYG/IEF).

Each theme → (optional Winsor) → (robust z or scaled ROC) → tanh → SMA smoothing.

Composite = weighted average → LSMA smoothing → compare to bands → dir ∈ {−1,0,+1}.

Rebalance & flips. Orders fire on your chosen cadence or when the sign of exposure changes.

Position size. exposure = clamp(TargetVol / realizedVol, maxLong/Short) × dir.

Note: The script also exposes Gross Exposure (% equity) and Signed Exposure (× equity) as diagnostics. These can help you audit how vol-targeting and caps translate into sizing over time.

Visuals & alerts

Composite line + columns (color/intensity reflect direction & strength).

Entry/Exit bands with green/red fills for quick polarity reads.

Hidden plots for each Theme if you want to show them.

Optional rebalance labels (direction, gross & signed exposure, σ).

Background heatmap keyed to Composite.

Alerts

Enter/Inc LONG when Composite crosses up (and on rebalance bars).

Enter/Inc SHORT when Composite crosses down (and on rebalance bars).

Exit to FLAT when Composite returns toward neutral (and on rebalance bars).

Practical tips

Start higher timeframes. Daily signals with Monthly rebalance are a good baseline; weekly signals with quarterly rebalances are even cleaner.

Tune Entry/Exit bands before anything else. Wider bands = fewer trades and less noise.

Weights reflect regime. If policy dominates markets, raise Monetary Policy weight; if credit stress drives moves, raise Risk Sentiment.

Proxies are swappable. Use UUP for USD, or futures-continuous symbols that match your data plan.

Futures vs ETFs. Quantity auto-rounds for futures; ETFs accept fractional shares. Check contract multipliers when interpreting exposure.

Caveats

Macro proxies can repaint at the selected signal timeframe as higher-TF bars form; that’s intentional for macro sampling, but test live.

Vol targeting assumes reasonably stationary realized vol over the lookback; if markets regime-shift, revisit volLook and targetVol.

If you disable normalization/winsorization, themes can become spikier; expect more hysteresis band crossings.

What to change first (quick start)

Set Signal Timeframe = D, Rebalance = Monthly, Z-score on, Winsor on (MAD).

Entry/Exit bands: 0.25 / 0.12 (defaults), then nudge until trade count and turnover feel right.

TargetVol: try 10% for diversified indices; lower for single stocks, higher for vol-sell strategies.

Leave weights = 1.0 until you’ve inspected the four theme lines; then tilt deliberately.

Hilly's Reversal Scalping Strategy - 5 Min CandlesHow to Use

Copy the Code: Copy the script above.

Paste in TradingView: Open TradingView, go to the Pine Editor (bottom of the chart), paste the code, and click “Add to Chart.”

Set Timeframe: Ensure the chart is set to 5-minute candles (TradingView: right-click chart > Timeframe > 5 Minutes).

Check for Errors: Verify no errors appear in the Pine Editor console.

Apply to Chart: Use a liquid crypto pair (e.g., BTC/USDT, ETH/USDT on Binance or Coinbase).

Verify Signals:

Green “BUY” labels and triangle-up arrows for bullish reversals (e.g., bullish engulfing, hammer, doji, morning star, three white soldiers, double bottom in a downtrend).

Red “SELL” labels and triangle-down arrows for bearish reversals (e.g., bearish engulfing, shooting star, doji, evening star, three black crows, double top in an uptrend).

Green/red background highlights for signal candles.

Backtest: Use TradingView’s Strategy Tester to evaluate performance over 1–3 months, checking Net Profit, Win Rate, and Drawdown.

Demo Test: Run on a demo account to confirm signal visibility and performance before trading with real funds.

Troubleshooting

If Errors Occur: If any errors appear in TradingView’s Pine Editor console (e.g., “Syntax error” or “Invalid argument”), please share the exact error messages to diagnose environment-specific issues.

Signal Overload: If too many signals appear, increase patternLookback to 15 or set volFilter = volume > volMa * 2.0.

Missed Signals: If signals are too rare, set useVolumeFilter=false or reduce patternLookback to 5.

Additional Features: If you need alerts, other indicators (e.g., EMA, RSI), or dynamic arrow sizing, please specify. Note that dynamic sizing caused errors previously, so I’ve kept size=size.normal.